The Levers of your Wealth - Part 1

If you could choose only one, which would you choose to maximize your wealth 15 years later?

Each year, your annual income grows 3% more than you expect.

Each year, your savings and investment (as a % of income) grow by 2% more upto a maximum of 66%.

Each year, your post-tax ROI grows by 0.5% until it reaches 10%.

The ideas of earning, saving and investing, and ROI (or levers as we call them here) given above are simple enough for a 10-year-old. But which one causes the most impact is not obvious because it involves compounding across a long period and different levers.

So what is the right answer?

Option 3, which focuses on ROI, is certainly the wrong answer for most investors. But the point of this article is not to belittle the importance of returns or prescribe a single answer. In fact, even for the same investor, the answer will change at different stages of investment and life.

In a four-part series, we will take you on a tour of numbers to show the change in your wealth due to each lever, namely, earning, investing, and ROI. If you still want to see which works best, see the table given in the last article

What is a lever?

Levers are a type of a simple machine used by humans since ancient times. See-saw, wheel-barrow, nut-cracker, and a pair of scissors are all examples of levers in which a little force produces a lot of impact. If you look at these examples closely, you will also see why the word leverage is derived from lever.

A simple example of a lever

A simple example of a lever

Levers are also used to describe ideas through which a little effort leads to a lot of impact. In this series, we look at how a change of a few percentage points in earning, saving, and investing could decide your portfolio as you near retirement.

To illustrate, you could do one or more of the following -

Lever 1 - Increase your income by working on a side project

Lever 2 - Track your expenses and invest a greater share of your income.

Lever 3 - Teach yourself investing and get greater returns

Just as you need asset allocation for your limited capital, you need effort allocation for each lever.

The numbers behind each lever

Since the impact of these levers can be best explained only through the numbers, let's look at the example of Rajesh, a 30-year-old man and young father who aims to be financially independent by the age of 50.

If he were to retire today, he would need a corpus which fetches him an interest of Rs. 18 lakhs per annum. Therefore, the target is to build an inflation-adjusted portfolio that provides this income in 2039.*

In the table below, we list the assumptions and describe each lever. We have given two types for each lever. For example, Lever 1 (Income) is divided into Lever 1.1 and Lever 1.2.

Table 1

Points to note -

These numbers have been chosen to reflect the average investor in India. While there will be variations, the assumptions are realistic enough to work for most people over the long-term.

Whether it is earnings or interest, all numbers are post-tax.

Although the official rate of inflation is 5.5%, the actual rate is always higher. For needs or goals like children’s education, medical expenses, or children’s wedding, the rate of inflation is much higher.

You can see the calculations here or input your own numbers by making a copy of the spreadsheet.

All assumptions are based on normal economic conditions and expected events. It is also assumed that there is no change in investment during the occasional economic downturn or a personal emergency.

Finally, life doesn’t work like numbers on a spreadsheet. These are projections, not predictions.

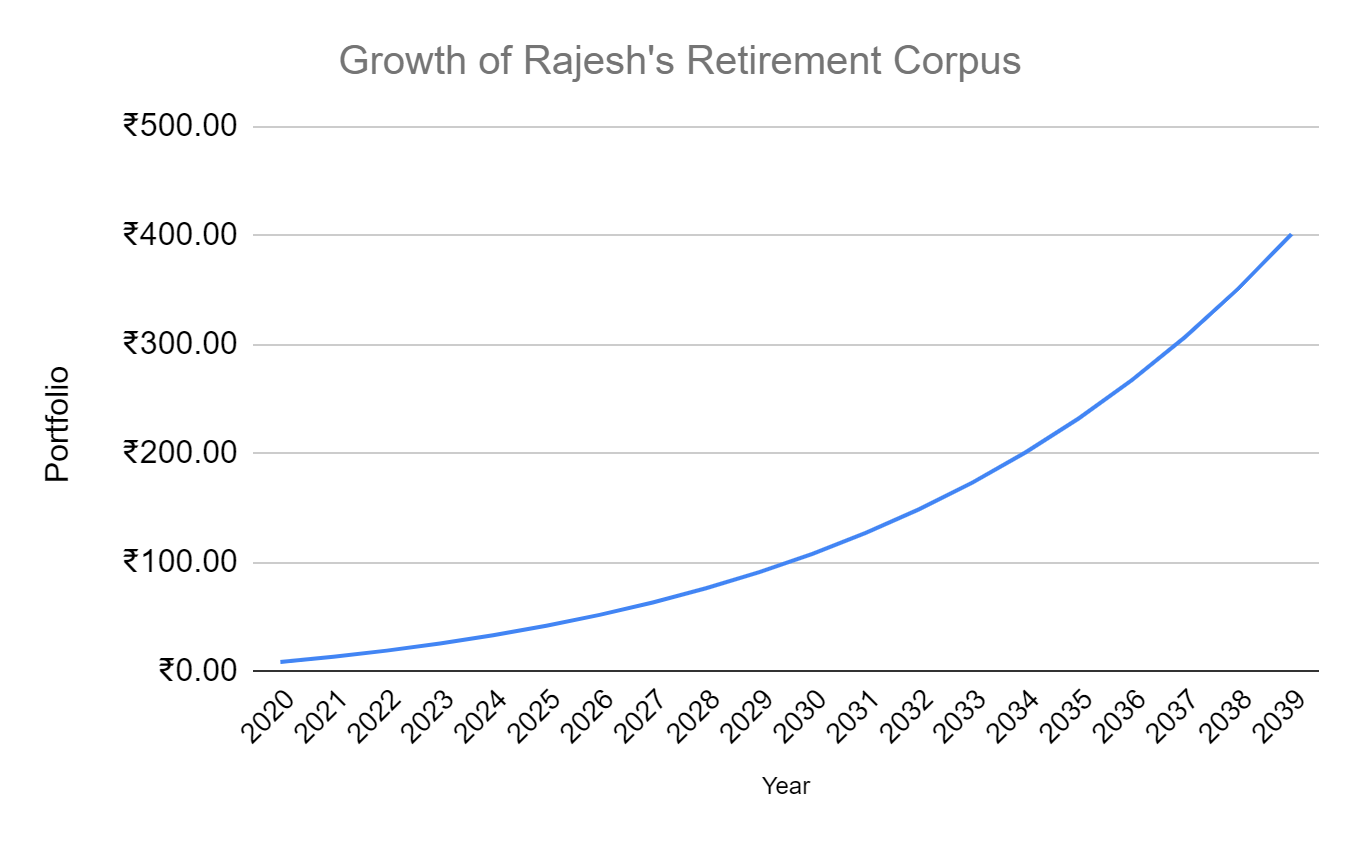

If nothing changes, Rajesh’s portfolio will be…

Graph 1

*All figures in lakhs

If Rajesh earns Rs. 9 lakhs annually, increases it by 10% per annum, invests 40% of it every year, and earns interest at 7.5%, his portfolio will grow to Rs. 4 crores in 20 years.

If Rajesh earns Rs. 9 lakhs annually, increases it by 10% per annum, invests 40% of it every year, and earns interest at 7.5%, his portfolio will grow to Rs. 4 crores in 20 years.

...Rs. 4 crores in the financial year 2039-40*, as given in graph above and table below.

Table 1 - When there is no change in earning, investing, or returns.

Note

* Rajesh is planning to retire 20 years from now in FY 2039-40. The numbers are given for alternate years after 2021 for the sake of brevity. To see the entire table, please click here.

**The salary hike is reflected only in the year after it is made.

***Rajesh has an opening balance of Rs. 4 lakhs

**** All figures in lakhs

But is Rs. 4 crores enough after 20 years? And if not, what should he do? We answer it in the next part of this series.

Other articles in this series -

Download the Wealthy Appto enjoy efficient Trading and Investing!

Welcome to Wealthy