Levers of Wealth, Part 2: ROI

In the previous article, we explained the importance of levers and how Rajesh’s retirement corpus will grow without applying any lever. In this article, we see how ROI grows that corpus.

To recap, this is where Rajesh stands financially today.

Salary = 9 lakhs per annum

Increment = 10% per annum

Previous Balance = Rs. 4 lakhs

% of salary invested = 40%

ROI = 7.5% post-tax, a little above the inflation rate of 7%

As we said earlier, his portfolio will be Rs. 4 crores in 20 years. But after accounting for inflation, this amount is Rs. 1.10 crores. In other words, the purchasing power of his portfolio in 2039 is equal to Rs. 1.10 crores today. At an interest rate of 7.5%, his portfolio will fetch him an income of Rs. 8.31 lakhs, way below his requirement of Rs. 18 lakhs.

Applying Lever 3: ROI

What if:

Rajesh learns to invest, gradually shifts most of his portfolio to equity, and increases his ROI by 0.5% until it reaches 10% per annum. Let us call this Lever 3.1.

Rajesh increases his ROI by 1% until it reaches 11% per annum? Let us call this Lever 3.2.

As given in the table below, this allows Rajesh to create only a little over half his retirement corpus after accounting for inflation. Clearly, focusing on ROI isn’t sufficient.

Table 1 - Change in portfolio by increasing ROI, all figures in lakhs

*All figures in lakhs

**To see the calculation, click here.

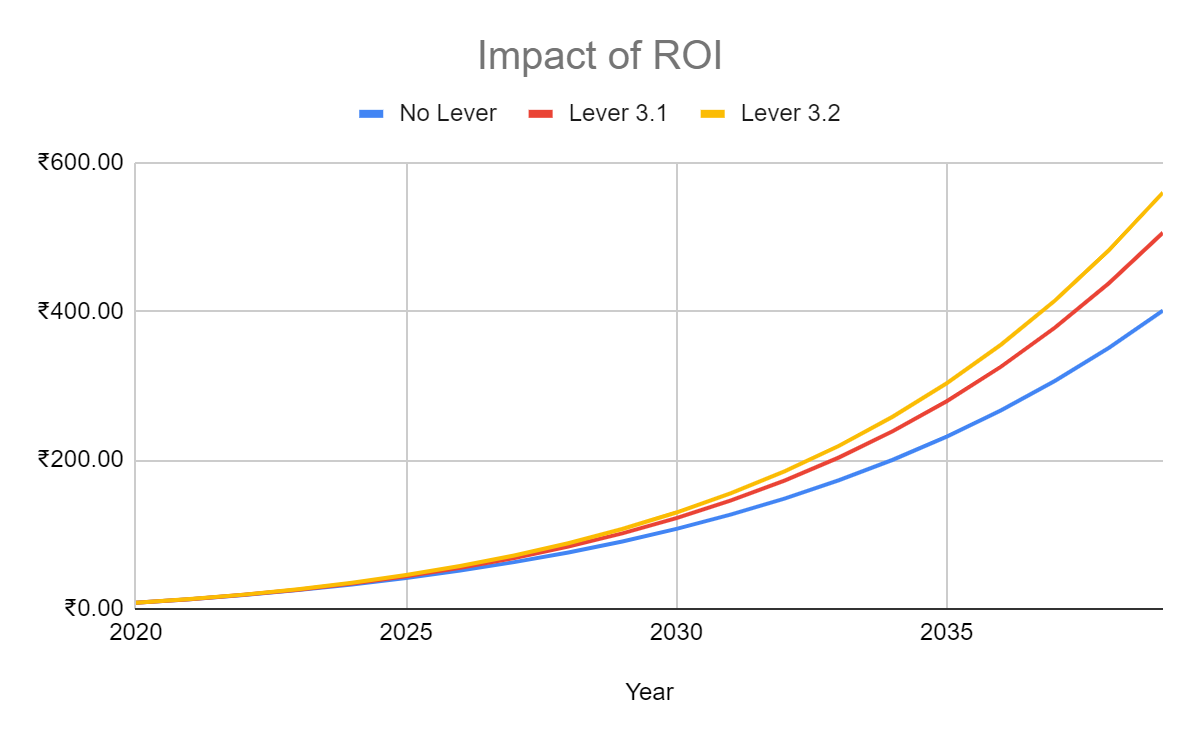

Graph 1

This graph shows the growth in the retirement corpus with each lever.

*All figures in lakhs

Growth under different rates of ROI: Note how the growth curve is near identical for the first 10 years.

Growth under different rates of ROI: Note how the growth curve is near identical for the first 10 years.

Why is it hard to increase the ROI?

Because it is risky, uncertain, and uncontrollable to some extent.

This is shown perfectly by the economic situation caused by Covid-19, a pandemic which originated in a foreign country and has (so far) spread to less than 0.1% of the population in India. And yet, it has led to layoffs, pay cuts, interest rate cuts, a stock market crash, and predictions of recessions. As always, those who chased returns and compromised safety have been hit the hardest, be it the investors in Yes Bank AT1 Bonds or Franklin Templeton Debt Mutual Funds.

If we were to talk specifically about certain products, Annuity Products and FDs of Public Sector Banks offer a post-tax return in the range of 6% to 7%. While government-backed products like EPF, PPF and Senior Citizens Savings Scheme offer better returns, they have long lock-in periods and investment limits. For any investor looking at post-tax returns over 9%, he/she cannot avoid equity, a product which is “subject to market risks.”

Secondly, as investors enter retirement or near their retirement age, they choose safety over returns and shift their portfolio towards debt and fixed-income products. In doing so, their returns are reduced.

When is ROI important?

One reason why the power of compounding is not evident is because it makes little impact in early years of investing.

To understand this, let us imagine scenarios in which Rajesh's portfolio fetches a high post-tax return of 14%, 17%, and even 20%. In such a case, how much time does it take Rajesh’s portfolio to reach the Rs. 1 crore mark? We answer it in the table below.

Table 2 - Time to grow portfolio to Rs. 1 crore

Even with a near-impossible, post-tax rate of 20%, it still takes over 8 years to reach a portfolio of Rs. 1 crore. In contrast, a very realistic ROI of 7.5% needs a slightly longer period of 11 years.

But the power of compounding starts showing only in the second decade. With a good ROI, your money generates more money even when you are sleeping. A poor ROI, especially one below inflation, slowly erodes it. To understand these, let us look at our earlier examples.

Even if Rajesh doesn’t add a single Rupee to his portfolio from 2039 to 2044, it still grows and brings him closer to his retirement corpus. Please see the highlighted row in the table below.

Table 3

Even when his portfolio remains untouched, it beats inflation and increases his retirement corpus.

ROI after retirement

During one’s earning years, the interest is reinvested in the portfolio while salary or other sources of income take care of other needs. But when one retires and other sources of income dry up, your ROI decides if and when you exhaust your portfolio, i.e bankruptcy.

Let us look at this with an example of two twin brothers, Ramesh and Mahesh. Both of them retire at the age of 50 with the same lifestyle, but slightly different portfolios.

Mahesh: Portfolio of Rs. 2.1 crores, ROI of 6.70%

Ramesh: Portfolio of 1.82 crores, ROI of 9.10%

If their annual expense of Rs. 6 lakhs (at age 50) grows by 7%, which of the two would exhaust their portfolio and when? The graph below answers the question.

Graph 2

*All figures in lakhs

Because the ROI of Ramesh's retirement corpus is 2.4% higher, it is able to stay ahead of inflation much longer.

Because the ROI of Ramesh's retirement corpus is 2.4% higher, it is able to stay ahead of inflation much longer.

Table 4

*All figures in lakhs

Observations

Both Ramesh and Mahesh eventually exhaust their portfolios.

By age 70, Mahesh’s expenses would exceed his income and he would be forced to withdraw from his portfolio. Before he turns 85, he would have depleted his portfolio completely. (See highlighted rows on left side).

The same would happen with Ramesh, except much later in life. His expenses would exceed his income at the age of 89 while he will run out of money by age 102. (See highlighted cells on the right).

Despite having a smaller amount, Ramesh’s portfolio is able to sustain him much longer due to a higher ROI.

Due to a lower ROI, which is 0.2% below inflation, Mahesh exhausts his portfolio earlier.

Summary

Among the 3 levers (earning, saving, and ROI), your ROI has the least impact in the initial years of investing.

In the later years, especially around the second decade, a small change in ROI will make a huge impact on your portfolio.

With increased life expectancy, someone retiring at 50 today has to account for a post-retired life longer than his/her working period. Without a good ROI, even a healthy retirement corpus could be reduced to nothing in a few decades.

Your ROI depends on the quality of your investments and the economy. While you have some control and knowledge of the former, you won't have enough of it for the latter.

In the next article, we will look at the impact of saving on your wealth

Other articles in this series

Download the Wealthy Appto enjoy efficient Trading and Investing!

Welcome to Wealthy