Levers of Wealth, Part 4: Income

In the earlier articles of this series, we looked at the role of ROI and saving. In this final part of this series, we look at the impact of your income on your wealth. Given below is a quick recap of all the three levers of wealth.

How much does your income matter?

Saying that your income plays the biggest role in your wealth would be as insightful as finding out that water is wet. However, it doesn’t explain the growth of your wealth, the role of your income, or the problems in focusing only on income. Let us illustrate this with a variant of our original question.

If you had to choose only one, which would you choose?

1) An increase of 1% in your income

2) An increase of 1.5% in your savings

3) An increase of 1.5% in your ROI

In this article, we will do a deep dive income to help you answer all these questions.

Assumptions

Income here refers to all your annual post-tax income including your salary. However, it will exclude any dividend or interest from your portfolio as it is assumed to get reinvested.

Whether you earn a salary or income from a business, it is assumed that you can increase it to some extent every year. In reality, this need not be true for some people such as government employees or those getting most of their income in the form of rent.

Most importantly, it is assumed that Rajesh doesn’t spend more because of the extra increment. Instead, the extra increment is invested fully.

So how much does your income matter?

To answer this question, let us turn to the same case study of 30-year-old Rajesh, who wants to build an inflation-adjusted portfolio of Rs. 2 crores and retire at the age of 50, i.e. 2039. This is the current state of his finances.

Salary = 9 lakhs per annum

Increment = 10% per annum

Previous Balance = Rs. 4 lakhs

% of salary invested = 40%

ROI = 7.5% post-tax, a little above the inflation rate of 7%

At the current rate, he would have saved around Rs. 2 crores by 2039. According to today’s rates, that would be around 77 lakhs, well below his target of Rs. 2 crores.

Applying the Lever of Income

To see the impact of an increase in his annual increment, let us look at the two levers.

- Suppose that instead of 10%, Rajesh’s income increases by 13% per annum, an extra 3% over his usual 10% increment. Let’s call this Lever 1.1

- Likewise, suppose that his income increases by 15% per annum. We will call this Lever 1.2.

While it is easy to say which will fetch the most wealth, let us see how much will be the retirement corpus under each.

Table 1 - Rise in retirement corpus by increasing increment

As given in the highlighted cells, an increase in increment makes a huge difference to your retirement corpus. An increase of 3% over the expected hike takes Rajesh close to his goal (Rs. 1.7 crores), while an increase of 5% takes him to Rs. 2.15 crores, well past his target of Rs. 2 crores.

Why income makes a big impact?

As evident from the table above, it is clear that a rise in annual income makes the most difference among all three levers. But why?

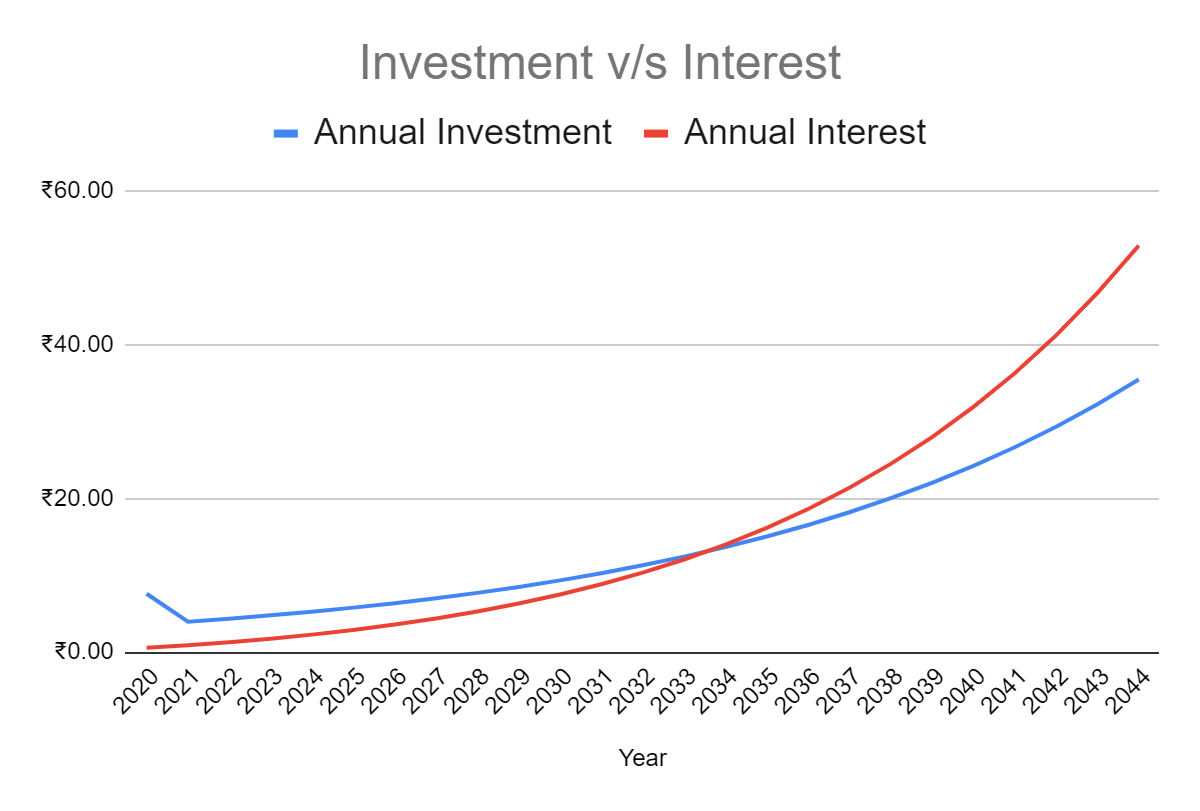

Firstly, your principal or amount invested makes the most difference in the early years. The effect of compounding is seen only after sufficient investment and time. Until then, the growth of your retirement corpus is decided largely by the amount you invest. This is seen by comparing the annual investment with annual interest.

Graph 1 - Investment v/s Interest

Graph 1 - Investment v/s Interest

In the above figure, the interest overtakes the annual investment around the year 2034.

Another way of showing this is what contributes to the growth of a portfolio. A portfolio grows through fresh investment and interest on previous investments. As the graph above shows, annual investment accounts for most of the growth in the initial years. However, the interest component eventually overtakes the annual investment.

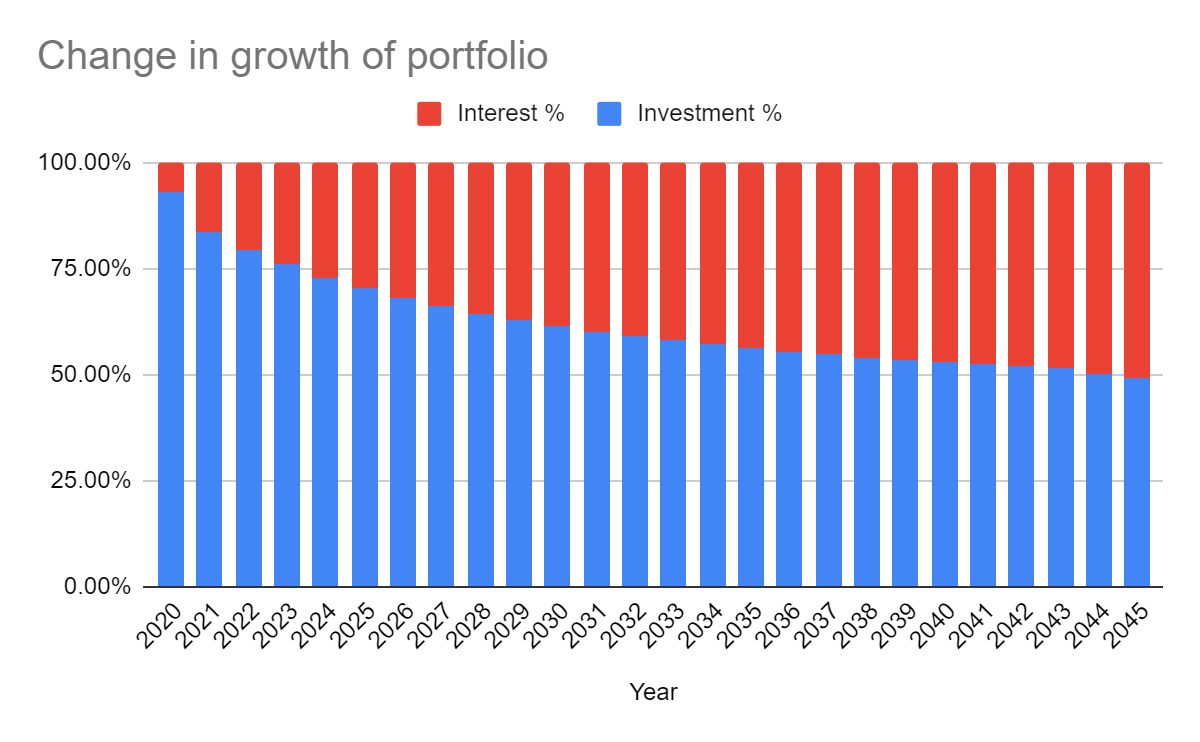

For the graph given below, it takes a little longer (in the year 2045, if Rajesh chooses to continue working until then) than the previous graph because it is for Lever 1.2 in which the income is increasing by 5% more than usual.

Even in Lever 1.2 (where income growth is the highest), the share of interest earned eventually overtakes that of investments.

Even in Lever 1.2 (where income growth is the highest), the share of interest earned eventually overtakes that of investments.

So which lever works the best?

Table 2 -

*All figures are given in lakhs

As a lever, income growth has the biggest impact in building a portfolio.

As given in the table below, Lever 3 or an increase in salary makes a bigger difference than saving or ROI. But that is no reason to put all your eggs in this basket. Although equity gives the highest return among all asset classes, any asset allocation will have a place for other assets. Likewise, you need to do an effort allocation for all your levers.

Putting it all together

The aim of this series is not to focus on one lever to make the most money. Instead, the aim is to spread your effort across all three levers to reduce your risk and help you build the wealth you deserve.

So let us look at the growth in Rajesh’s wealth (or retirement corpus, in this case) if you worked a little on all three levers. In other words, what will be the impact if you slightly increased your salary, savings, and returns?

Lever 1, Salary - Rajesh increases his annual increment by 2% from 10% to 12%

Lever 2, Saving & Investing - Rajesh saves 1.5% more year-on-year up to a maximum of 66%

Lever 3 - Rajesh increases his post-tax ROI by 0.5% per annum until a maximum of 10% per annum

Result? As given in the table below, Rajesh is able to build an inflation-adjusted corpus of Rs.2.25 crores, more than his goal of Rs. 2 crores. With this sum, he should be able to retire 20 years from now.

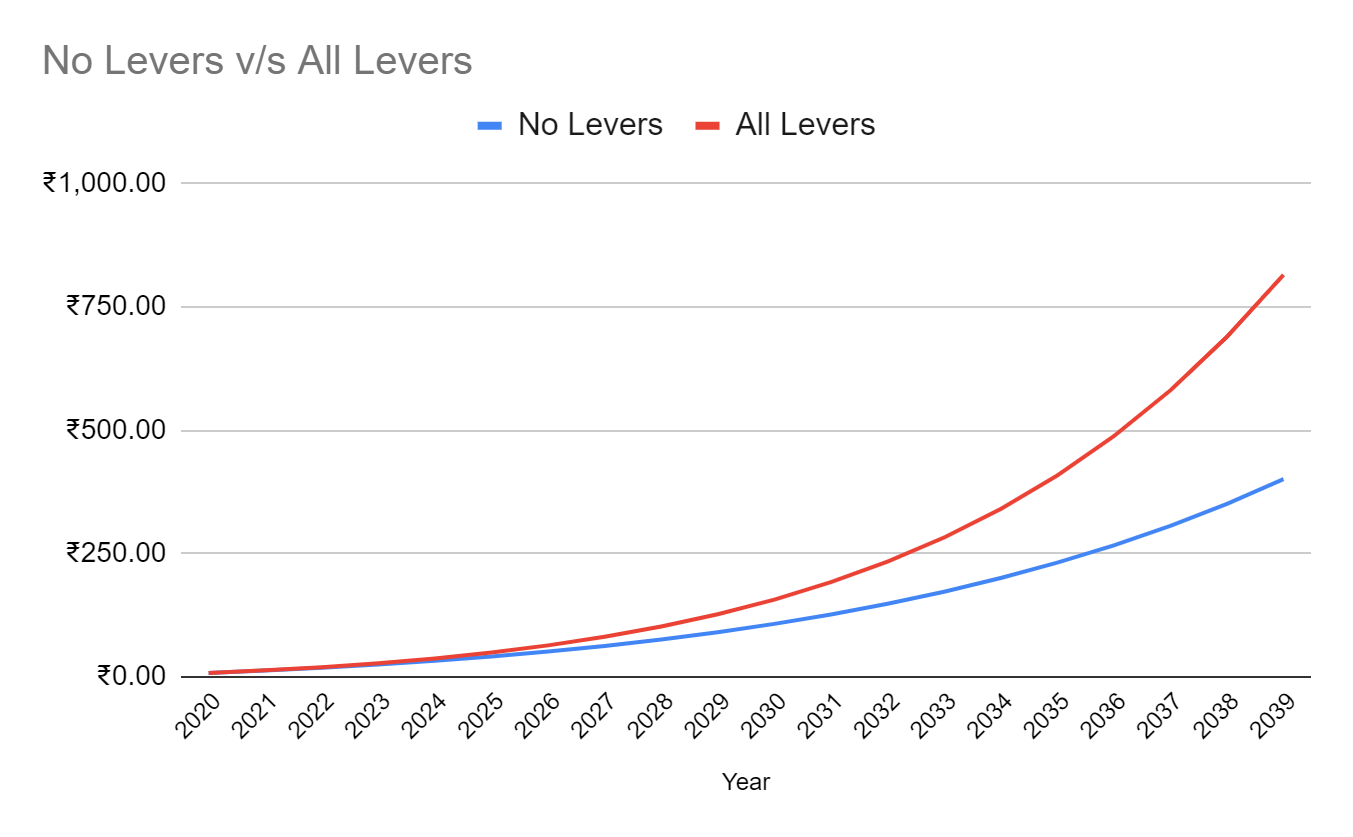

As given in this graph and table below, a small change in each lever doubles your portfolio over 20 years.

As given in this graph and table below, a small change in each lever doubles your portfolio over 20 years.

Table 3 -

*All figures are given in lakhs

Summarizing all three levers

Previous articles in this series -

Download the Wealthy Appto enjoy efficient Trading and Investing!

Welcome to Wealthy