“The index composition is very different today”

Nifty P/E - Is 40 the new 30?

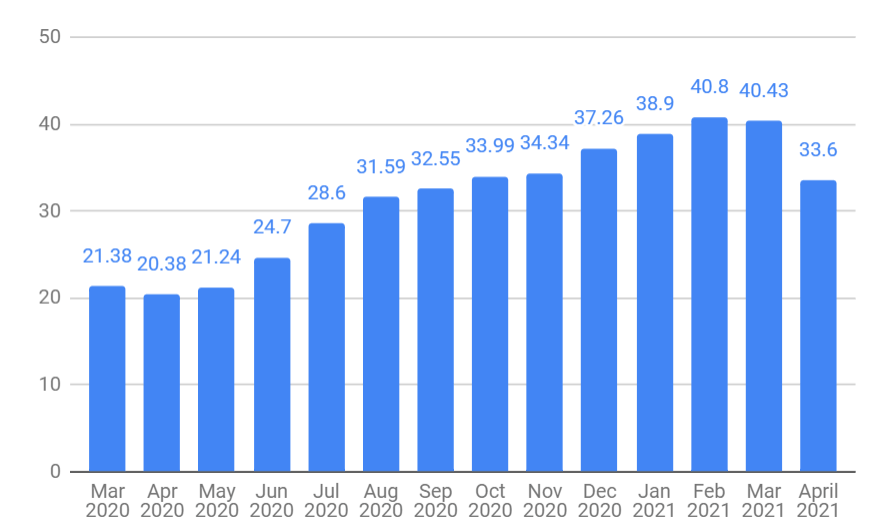

After the crash of March 2020, the Nifty PE kept rising and breached the 30-mark for the first time. However, it didn't stop there and touched 40 for the months of February and March this year. Like the planet, it seems like the Nifty PE is also warming (see graph given below).

Note: The PE fell in April 2021 due to a reporting change. Read the interview below to know more.

Why is it important?

Unlike the Nifty or Sensex, the P/E is a ratio. Secondly, it indicates how much investors are willing to pay for future returns.

Considering the low earnings and ample liquidity, it might seem that a Nifty P/E of 40 in FY21 is equal to 30 in FY20. But as Dev Ashish aka Stable Investor explains in this interview, the increase is caused by the change in companies comprising the index. Read on to know how a change in reporting earnings has caused a fall in PE, or how the PE has increased due to a change in constituents of the Nifty.

Note: The answers given shouldn’t be construed as investment advice. You are advised to consult a professional before making any investment decision.

1) Your Nifty50 heat-map suggests that the P/E ratio was warming long before the pandemic struck. For instance, it was under 20 for 12 out of the first 15 years of this century. But since 2014, there hasn't been a single one like that. In fact, it has steadily increased.

What does this tell you about our economy and market?

Compared to 2000 or 2005, the index composition is very different today. Since it is now managed actively, the weightage of sectors/industries in the index changes over time.Now all sectors within the index aren’t the same. So if the index has a large number of companies with low P/E in general, then the Index P/E will be accordingly low. If the share of high-P/E companies increases in the index, the same impact will be seen on the Index P/E as well.

For example, let’s assume the index is made up of 5 companies equally. In the first year, these companies are from low-P/E industries with a P/E of 11, 12, 13, 14 and 15 during normal (fair value) years. Hence, the index P/E is 13. Now in a bull market, the P/E of these companies rises to 17, 18, 19, 20 and 21. Thus, the Index P/E also rises to 19.

Now after about 10+ years, the index constituents have changed. The companies now belong to high-P/E industries and hence, have P/E of 21, 22, 23, 24 and 25 during normal (fair value) years. The index P/E is 23. Now in a bear market, the P/E of these companies falls to

17, 18, 19, 20 and 21. The index P/E comes down to 19.

As you can see, the index P/E is 19 in both cases. But the first P/E of 19 shows overvaluation, while the second P/E of 19 shows undervaluation. When comparing Index P/E across years, the definition of fair, under and overvaluation will change to some extent due to the nature of the companies in the index.

Note - From 1st April 2021, Nifty P/E has shifted to consolidated mode from the earlier standalone mode. So the reported P/E will now be lower going forward as consolidated EPS is higher than standalone one. I have written about this some time back here.

2) In the first three months of this year, the Nifty P/E ratio has averaged over 40. Has the definition of a "paisa-vasool" P/E ratio changed for the average investor? Or is 40 the new 30, or even 25?

This has been answered to some extent in the first question.Since the second half of March, the P/E has been on an upward journey. But the rise in P/E valuation wasn’t just because of the markets moving up.

In the P/E Ratio, the Market Price (Nifty50 Index level) is the numerator and Earnings per share (EPS of Nifty50) is the denominator. So normally, the ratio will increase if the index (numerator) increases and/or if the EPS (denominator) falls.

Right now, both are happening. Index (numerator) has risen from its lows while EPS (denominator) has also fallen in the last few months.

Index rising was fine. But why is EPS falling?

The lower revenues (and hence, lower earnings) during the lockdown led to a steady decline in underlying EPS of Nifty50 companies . And since EPS considers trailing 12 months earnings data, the lockdown impacted the months of April/May/June which were then part of the trailing 12 months data being considered.

3) Is the increase in P/E ratio an inevitable outcome with more investors entering the market every year? What does the history of other economies tell us?

As seen in the first answer, at times, expansion of P/E will be due to increase in bullishness of investors and their willingness to pay a higher multiple. But many times, P/E expansion is due to the change in nature of companies that are part of the index (like more high P/E

companies joining the index while low P/E ones being ejected out).

4) You have written that this ratio shouldn't be taken at face value. Does it now mean that investors will have to look more carefully for opportunities and slice the data on sector, weightage, period, and other factors?

Yes, one should never make the mistake of looking at index P/E in isolation. There are several components within the P/E analysis itself; more importantly, there are several other factors (other than P/E ratio) that must be assessed before making any investment

decisions.

But given the nature of P/E (as discussed in answers 1 and 2), the comparative high valuations cannot be simply written off. One needs to think deeper if one is investing directly.

5) For the average investor, is there any reason to invest differently in the next 12 months?

If the investment is for the short-term (around 3 years), then it’s best to be debt-heavy. Plain and simple. But if the goal is long term and several years away, (say around 10 years) then following prudent asset allocation is the key.Suppose a few months back, an investor’s equity:debt ratio was 60:40 for a long term investment portfolio. But due to the run up in equity markets, it is now at 70:30 in favor of equity. So it might be a good time to rebalance the portfolio back to 60:40 and rope in some of the profits that have come quickly over the last year. This will also help if markets correct from here due to any reason whatsoever.

6) What should an investor keep in mind?

It might be tempting to go after the best performing stock or fund of the last 12 months, this greedy strategy may not work. For most, it’s best to pick a few financial goals, figure out a reasonable, non-adventurous asset allocation for the goal, find out the investment required, and take action to implement the plan.Trying to time the market, or find the next multibagger or other such fool’s errands are good only for a small part of one’s portfolio. But the core of your portfolio should be goal-based and properly asset allocated at all times. That is the way to go if you want to increase the probability of goal achievement and have a real shot at favorable portfolio outcomes.

Download the Wealthy Appto enjoy efficient Trading and Investing!

Welcome to Wealthy

OR

Curated Investing

Completely Digitalised

Bank Grade Security

Help Centers

Latest Blogs

Kusumgar IPO: Issue Details, Timeline, Business and FinancialsAdvit Jewels IPO: Price Band, Lot Size, Timeline, and DetailsTurtlemint Fintech Solutions IPO: Price Band, Lot Size, Timeline, and DetailsClay Craft India IPO: Price Band, Lot Size, Timeline, and Key DetailsHexagon Nutrition IPO: Details, Price Band, and Financials